전체 트랜스크립트

트랜스크립트 불러오는 중…

https://www.youtube.com/watch?v=EP4ptjamPYA

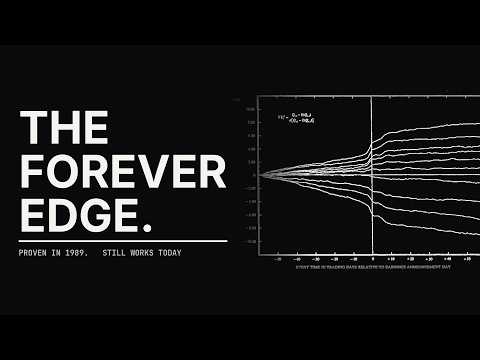

TL;DR — Institutional traders have been leveraging a market inefficiency known as Post-Earnings Announcement Drift (PEAD) for decades, quietly making billions. This phenomenon, where stock prices continue to move in the direction of an earnings surprise for weeks after the announcement, contradicts efficient market theory and is well-documented in academic finance. The video outlines how to extract a simple, mechanical trading strategy from this research, emphasizing accessible data and tools for retail traders.

Takeaway — Retail traders can exploit well-documented market inefficiencies like PEAD by following academic research, using accessible data, and employing mechanical trading strategies, thereby gaining an edge previously reserved for institutions.

요약 — 기관 트레이더들은 수십 년 동안 '실적 발표 후 주가 흐름(PEAD)'이라는 시장 비효율성을 활용하여 조용히 수십억 달러를 벌어왔습니다. 실적 서프라이즈 발표 후 몇 주 동안 주가가 그 방향으로 계속 움직이는 이 현상은 효율적 시장 가설에 위배되며 학술 금융 연구에서 잘 문서화되어 있습니다. 이 영상은 소매 트레이더들이 접근할 수 있는 데이터와 도구를 사용하여 이 연구에서 간단하고 기계적인 거래 전략을 추출하는 방법을 설명합니다.

결론 — 소매 트레이더는 PEAD와 같은 잘 문서화된 시장 비효율성을 학술 연구를 따르고, 접근 가능한 데이터를 사용하며, 기계적인 거래 전략을 채택함으로써 활용할 수 있으며, 이를 통해 이전에 기관 전유물이었던 이점을 얻을 수 있습니다.